The AI Trade Is Not Falling Apart — The Market Is Separating the Likely Winners

AI demand is still strong. What has changed is that investors now want to know who is funding the buildout, who is supplying it and who can turn it into cash.

The recent weakness in chip and memory stocks does not mean the AI trade is over. It means the market is becoming more selective.

During the first half of the year, nearly every company connected to AI moved higher. Chips, memory, servers, networking, cooling, power and data-center stocks were treated as one enormous winning trade.

Now investors want proof. They want companies that can turn AI demand into revenue, strong margins and free cash flow without spending themselves into a hole.

Why “Capex Light” Matters

Capex is the money companies spend on long-term infrastructure.

AI requires enormous investment in data centers, chips, servers, cooling, networking and electricity. The companies funding those projects may earn strong returns, but they must spend the money first and prove the payoff later.

A capex-light company can benefit from the AI boom without carrying the full cost of building it.

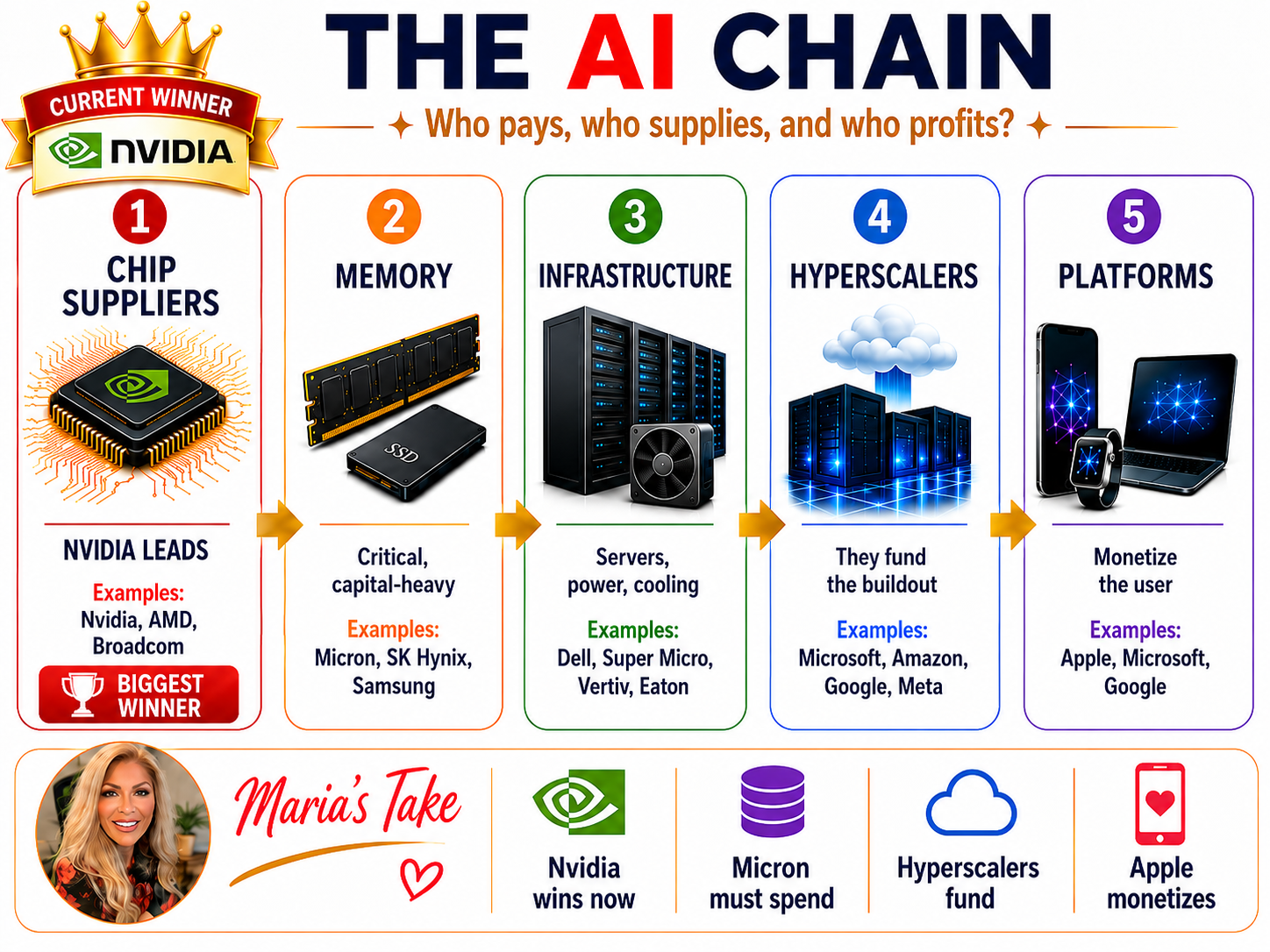

The key question is simple: Who is paying for the AI boom, and who is getting paid? |

Here Is the Breakdown of How It All Fits Together

Microsoft, Amazon, Google and Meta are financing much of the buildout through data centers and computing capacity. Nvidia supplies the processors, systems and networking equipment. Micron supplies the advanced memory those AI systems need to operate at full speed.

Data-center operators, power companies, cooling providers and server manufacturers build and maintain the physical infrastructure. Apple sits closer to the consumer, using AI to improve devices, applications and services it already controls.

They are all part of the AI trade, but their economics are very different. Some are paying to build it, some are selling the equipment and others are trying to monetize AI through an existing platform. That is what the market is sorting out.

Nvidia Supplies the Boom

Nvidia remains one of the clearest AI beneficiaries because it sells the processors, systems and networking equipment needed to build AI infrastructure.

The hyperscalers spend billions expanding data centers, while Nvidia earns revenue from much of that spending. It does not have to own every facility, negotiate every power agreement or operate every cloud platform. It sells the tools that make the buildout possible.

Nvidia is not risk-free. It must continue delivering tremendous growth while defending its lead against custom chips, competitors and export restrictions. Still, its role is straightforward: others are financing the construction boom, and Nvidia is supplying it.

Micron Must Spend to Meet Demand

Micron is benefiting from rising demand for high-bandwidth memory, but memory manufacturing is far more capital-intensive.

Micron reported approximately $7.1 billion in quarterly capital expenditures as it invested in technology, production and additional supply.

That spending may be necessary to meet AI demand, but memory remains cyclical. Pricing, supply and customer demand can change quickly. Investors will continue watching:

- Capital expenditures and production capacity

- Future memory pricing

- Customer concentration

- Whether profits justify the spending

I still believe memory is one of the most important parts of the AI buildout. Nvidia's chips cannot perform at their full potential without advanced memory. But Nvidia and Micron are not the same trade: Nvidia sells into the boom, while Micron must spend heavily to support it.

The Cloud Builders Must Prove the Returns

Microsoft, Amazon, Google and Meta are spending massive amounts on AI infrastructure. Their challenge is not proving that AI matters. It is proving that customers will pay enough for AI products and services to justify the investment.

The market will watch cloud revenue growth, AI adoption, margins, capital spending, free cash flow and return on investment.

These companies may become some of the largest AI winners, but the spending must eventually produce measurable returns. Investors will not give them unlimited time or unlimited money.

Data Centers, Power and Servers Still Matter

AI cannot expand without data centers, electricity, cooling, servers and networking. Those companies can continue benefiting from the buildout, but growth may require constant investment.

Enormous demand does not guarantee strong shareholder returns if expenses rise faster than profits. This is the difference between having AI exposure and having strong AI economics.

Apple Owns the Consumer

Apple offers a different way to participate in AI. It is not trying to win the data-center arms race; its advantage is the consumer ecosystem it already controls.

Apple can use AI to improve the iPhone, Mac, applications, search, services and productivity tools. It needs those features to make its devices more useful, strengthen customer loyalty and eventually drive upgrades or greater service usage.

Apple still has something to prove, but it already owns the customer relationship. That gives it a potentially less capital-intensive path to AI profits.

Maria's Bottom Line

As a long-time Nvidia bull, this breakdown confirms why I still see Nvidia as the biggest winner in the AI buildout. It is not simply selling picks and shovels — it is providing much of the technology the entire system depends on.

I will continue watching Micron, Apple, the hyperscalers and the companies powering the data-center boom. But for now, Nvidia remains the company I believe is best positioned to get paid as everyone else races to build.

|

|