Issue No. 17 • Friday June 12, 2026

|

|

THE TRADING ADDICT

NEWSLETTER

by Maria Helmick

» Story No. 1 of 2 · IPO Watch

Tap the image to view full size

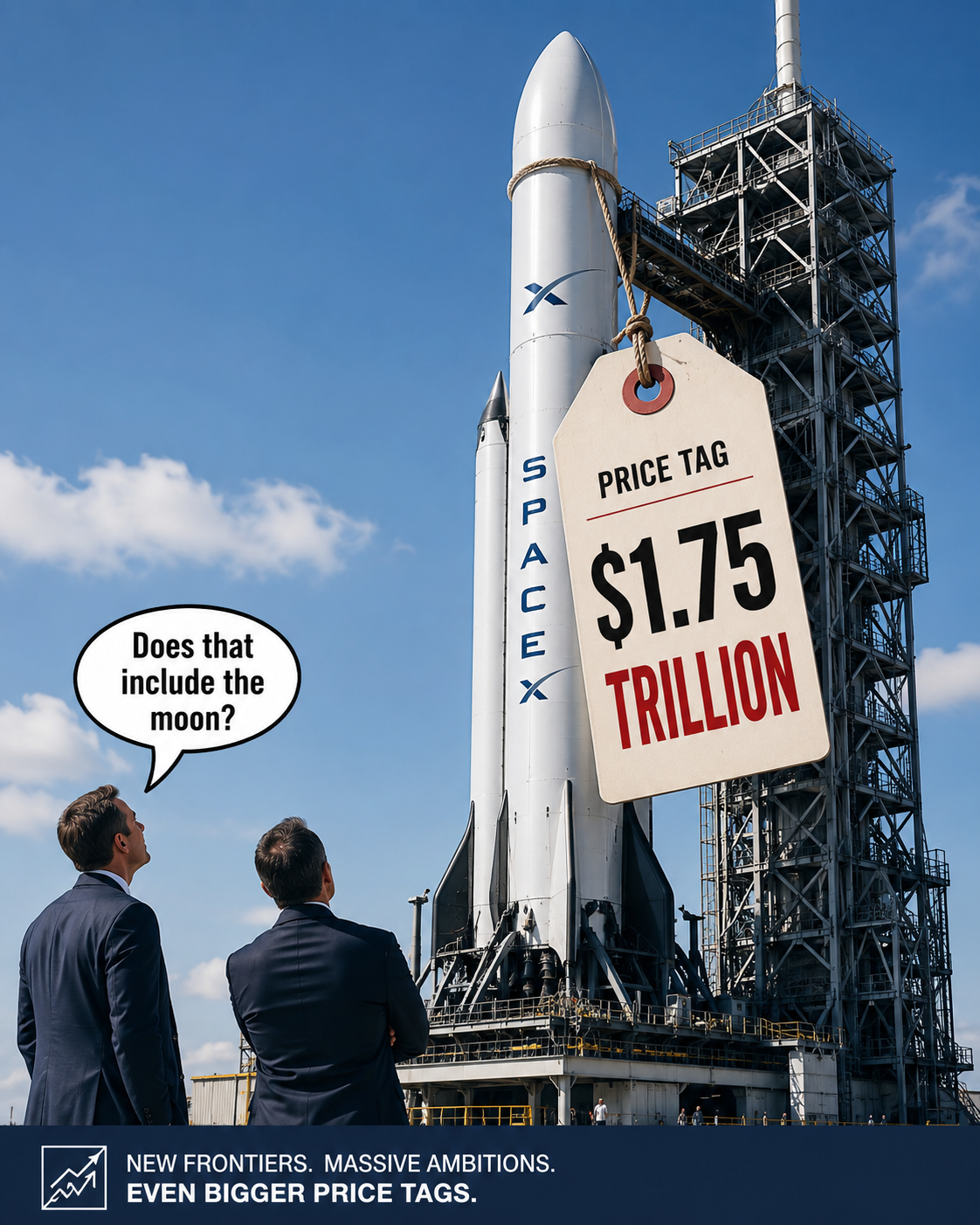

SpaceX IPO: Wall Street Wants In — But Is $1.75 Trillion Too Rich?

A world-class company is coming public with world-class demand. The question is whether investors are already paying for perfection.

SpaceX may be one of the most exciting companies to ever come public.

The expected IPO price is $135 per share, valuing the company near $1.75 trillion. That puts SpaceX in rare air before it even starts trading.

There is no debate about the business. SpaceX changed the economics of rocket launches, built Starlink into a global satellite internet giant, and created a lead that competitors may need years — and billions of dollars — to chase.

But investors have to ask the harder question: Is SpaceX still an opportunity at this price, or is it already priced like everything goes right?

Starlink Is Carrying the Financial StoryThe rockets get the headlines, but Starlink is the engine investors are watching. Starlink now has more than 10 million customers and reportedly generated about $1.19 billion in operating profit in the first quarter of 2026. SpaceX has a major advantage because it launches its own satellites on its own rockets. That keeps costs lower, speeds up expansion, and makes it harder for competitors to catch up. |

The concern is pricing. As Starlink expands into lower-cost markets, average revenue per customer has been moving lower. That means the next leg of growth likely needs to come from more subscribers, enterprise customers, government contracts, defense work, and new communication services.

Big Money Is Already Lining UpThis IPO is not acting normal. According to The Wall Street Journal, BlackRock has reportedly placed an order to buy at least $5 billion worth of SpaceX shares. Other large asset managers have reportedly submitted major orders too, and Bloomberg has reported that some institutional bids may be worth $10 billion or more individually. |

That does not guarantee the stock works from day one. But it does tell you something important: the biggest money managers in the world want exposure to SpaceX.

This is not just retail hype. This is institutional money trying to get a seat at the table before the public market even opens.

The Upside Is Obvious

The bull case is easy to understand.

SpaceX dominates commercial launches. Starlink keeps growing. Government demand for satellite communication, defense technology, and space infrastructure is only getting bigger.

Then there are the future opportunities: direct-to-cell service, military networks, space-based data infrastructure, and whatever comes next from a company that has already proven it can create new markets.

If SpaceX keeps executing, this could become one of the most important infrastructure companies in the world. Few businesses have this combination of technology, scale, brand power, and long-term optionality.

But the Price Tag Matters

The risk is not the company. The risk is the valuation.

At a valuation near $1.75 trillion, investors are already paying for years of future success. SpaceX will need Starlink to keep expanding, launch dominance to remain intact, margins to hold up, and new businesses to turn into real revenue.

That can happen. But if growth slows, competition increases, regulations tighten, or the market simply decides the valuation is too rich, the stock could struggle even while the company remains excellent.

Great companies can still be bad trades when the price gets stretched.

Cathie Wood Wants In TooCathie Wood and ARK Invest have also shown interest in buying SpaceX shares. That fits her disruptive-innovation playbook. SpaceX checks nearly every box: space, satellite internet, defense technology, autonomy, AI infrastructure, and long-term platform growth. Her interest adds another high-profile name to a growing list of buyers. |

Maria’s Bottom LineSpaceX looks like an elite company. The business is real. The moat is real. The demand is real. When BlackRock is reportedly putting in a $5 billion order, other institutions are lining up with even larger bids, and Cathie Wood wants exposure, Wall Street is clearly paying attention. But investors still need to separate the company from the stock. At $135 per share and a valuation near $1.75 trillion, SpaceX is not coming public cheap. Buyers are paying upfront for years of growth in Starlink, defense, communications, and future space infrastructure. This could absolutely become a generational winner. But at this price, it also has to execute like one.

|

Educational only. Not financial advice.

|

Apply to The AI Trading Institute Learn How We Actually Build, Run, and Update Our AI Trading Robot PhilThe next class starts Monday, June 29. The waitlist closes Monday, June 15, 2026, at 5:00 PM Eastern Time — just 3 days away. Seats are limited and the group is curated. Rob reviews every application personally and does a personal interview with every applicant. APPLY AT MATHMAKESMONEY.COM → |

» Story No. 2 of 2 · Earnings & Leadership

Tap the image to view full size

Once Again, Same Story, Different Stock: Adobe Beats — And Still Gets Punished

Adobe delivered the kind of quarter investors normally want to see: record revenue, an earnings beat, strong AI growth and higher full-year guidance. It still was not enough.

The company reported quarterly revenue of $6.62 billion, up 13% from last year, while adjusted earnings came in at $5.96 per share. Adobe also said its AI-first annual recurring revenue climbed above $500 million, more than tripling year over year.

On the surface, this was a solid report. Adobe beat expectations on both revenue and earnings and raised its full-year outlook. That should have been good news for shareholders.

The Numbers Were Not the Problem

Then came another headline investors did not want to see. Adobe CFO Dan Durn is leaving the company on June 15 to pursue another professional opportunity. Steve Day, a 20-year Adobe finance veteran, will step in as interim CFO.

That adds another layer of leadership uncertainty. CEO Shantanu Narayen has already announced that he will transition out of the CEO role once Adobe names a successor, while remaining chairman of the board.

The result was the same story investors have seen with several technology companies this earnings season: strong results, decent guidance and a stock that still goes down.

Wall Street Wanted More

Adobe continues to produce real revenue and earnings, and its AI business is growing quickly. But Wall Street remains skeptical about whether the company can protect its position as new AI tools enter the creative-software market.

That means even a good quarter may not be enough until Adobe proves that AI will strengthen the business rather than disrupt it — and until investors become more comfortable with the leadership changes.

Maria’s Bottom LineI may be collecting rent on Adobe for a while through covered calls. The business delivered, but the stock continues to disappoint. Rather than simply sit and wait for Adobe to recover, I may sell covered calls against my shares to bring in premium and gradually lower my cost basis. The key is choosing a strike where I would still be comfortable selling the shares if the stock rebounds. For now, the plan is simple: hold the stock, collect premium and let Adobe work its way back. |

Educational only. Not financial advice.

|

Math Makes Money TRADES OF THE WEEK0DTE SPX • $30K SCHWAB ACCOUNT Week of June 12, 2026 |

|

All trades 0dte SPX iron condors on the $30K Schwab account. MEIC = Multiple Entry Iron Condor. 50W = 50-wide wings. 95% = stop loss on short leg. No profit target — let trades expire. |

|

Risk Warning At the time of this writing, we plan on entering most of these trades, but they are part of a much greater and larger trading program and should be considered for educational and entertainment purposes only. Not financial advice of any kind. Trading involves substantial risk and is not suitable for every investor. You can lose some or all of your money. Nothing here is financial advice or a recommendation to buy, sell, or copy any trade. Do not copy trades blindly. Do your own due diligence, understand the risk, and make decisions based on your own account, risk tolerance, and financial situation. |

Join the Live Daily ShowLive trading. Come join us to watch live trading with the AI robot and ask Maria and Rob questions in the chat. A community of trading addicts. JOIN THE TRADING ADDICT → |

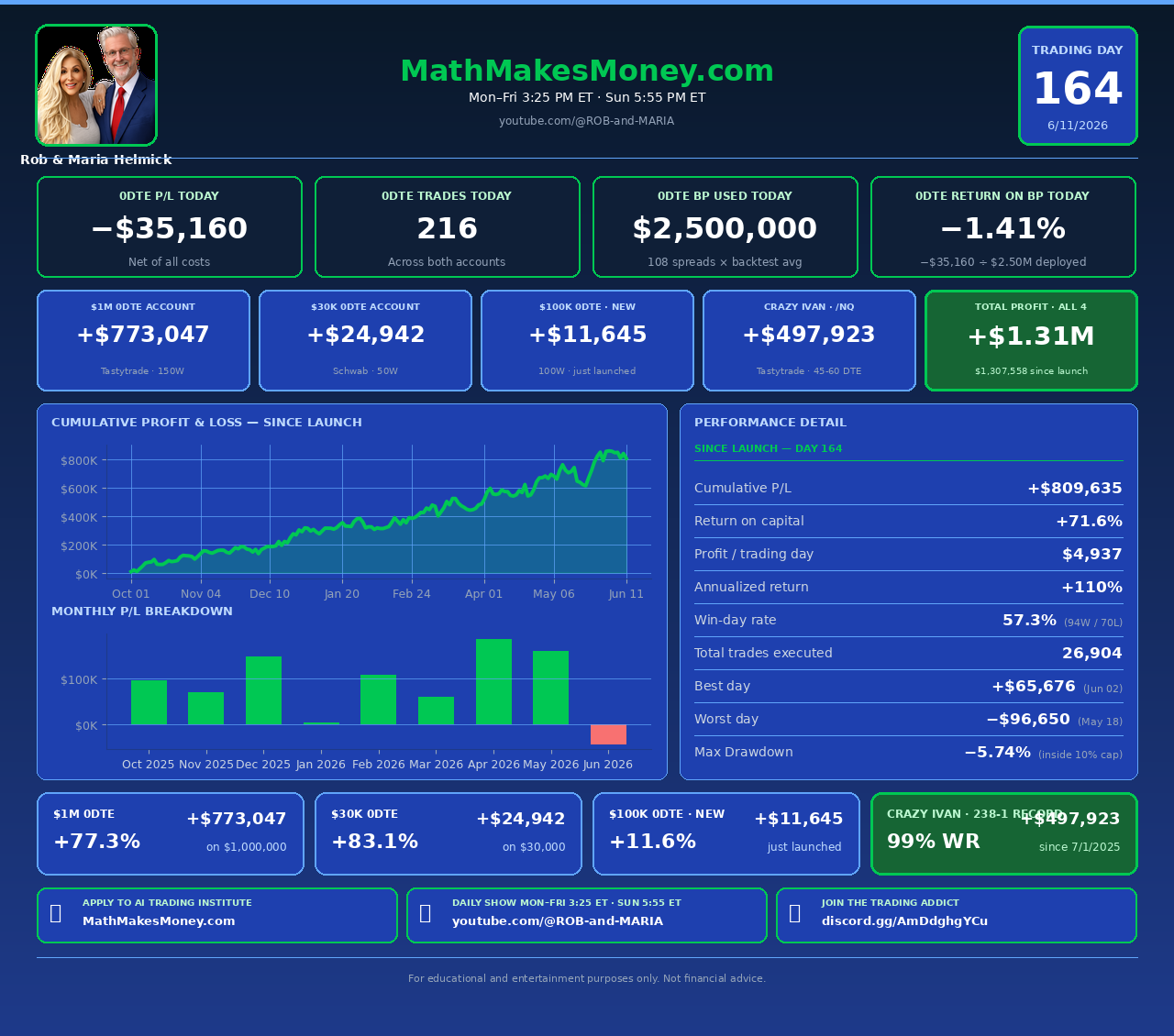

» Daily Trading Update · Day 164 · Tap for live dashboard

Here is how our AI trading robot Phil performed today.

|

» Quick Short · Watch on YouTube Today’s 60-Second Recap from Rob ► WATCH ON YOUTUBE

► WATCH ON YOUTUBE

|

Trade small, trade often.

Trade with your head, not with your heart.

Math Makes Money.

Get a fill, Phil.

— Maria

Math Makes Money · AI Trading Holdings LLC