Issue No. 16 • Thursday June 11, 2026

|

|

THE TRADING ADDICT

NEWSLETTER

by Maria Helmick

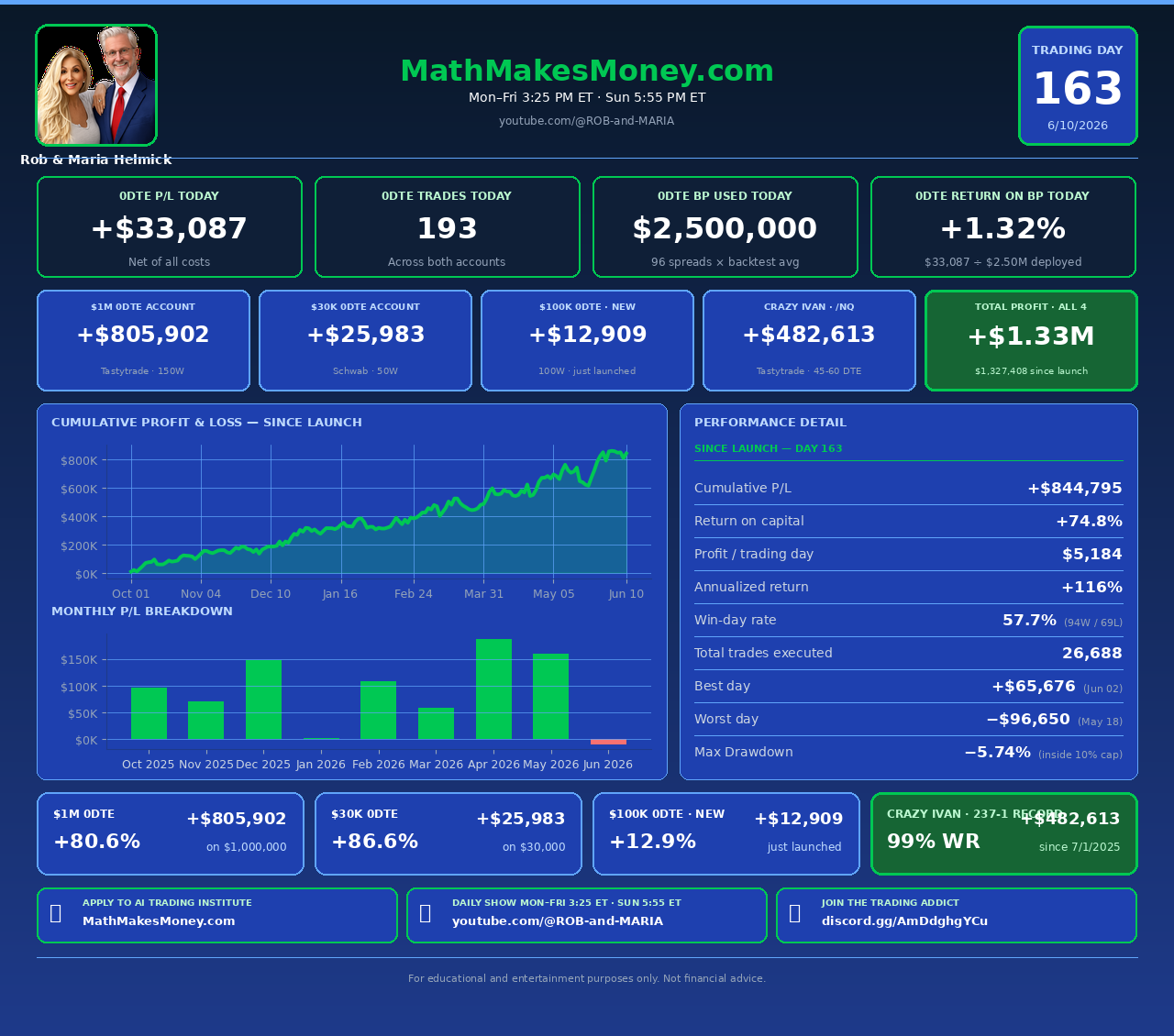

» Daily Trading Update · Day 163 · Tap for live dashboard

Here is how our AI trading robot Phil performed today.

» Trades of the Week are at the end of the Newsletter «

» Story No. 1 of 2 · Oracle Earnings

Tap the image to view full size

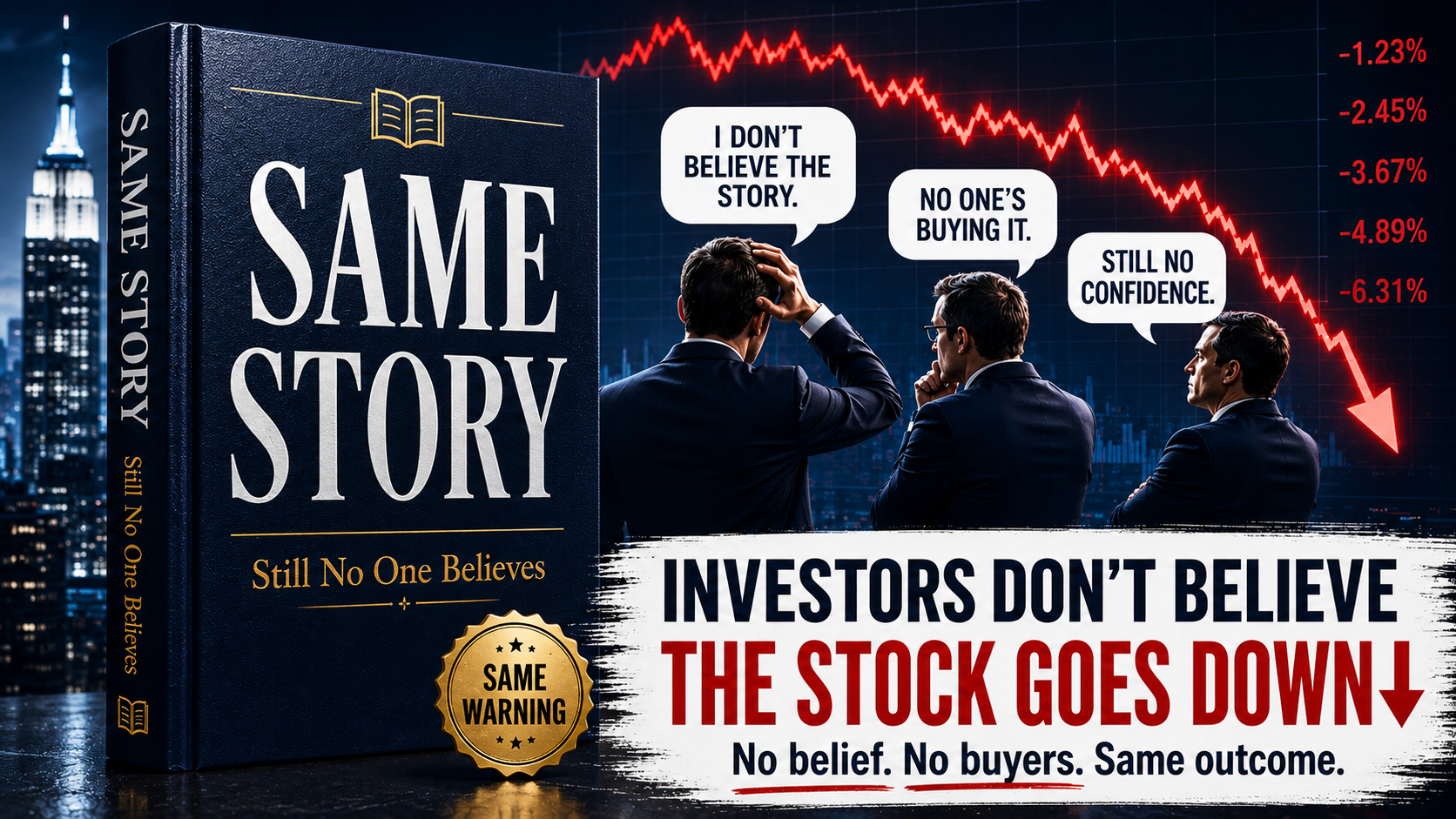

Same Story, Different Stock

Oracle beats expectations, but Wall Street focuses on the cost of the AI buildout.

Oracle put up a strong quarter, but Wall Street still found something it didn’t like.

The company reported record quarterly revenue of $19.18 billion, up 21% from last year and slightly ahead of estimates. Adjusted earnings came in at $2.11 per share, well above the $1.96 Wall Street expected.

|

The Big Growth Number Oracle Cloud Infrastructure revenue jumped 93% to $5.8 billion, while Oracle’s backlog of signed contracts climbed to a massive $638 billion. |

Those are impressive numbers.

The Problem: AI Growth Is Expensive

Once again, investors looked past the earnings beat and focused on how much money Oracle is spending to build out its AI business.

Oracle spent $55.66 billion on capital expenditures during fiscal 2026. That heavy spending pushed free cash flow to a negative $23.69 billion for the year.

The company now expects to raise roughly $40 billion in fiscal 2027 to help fund more data centers and AI infrastructure. That includes the previously announced $20 billion stock offering.

|

That was enough to send Oracle shares down about 6% after hours. |

Wall Street Wants Proof

The concern is simple: Oracle’s cloud business is growing fast, but investors are not yet convinced it will be as profitable as the company’s traditional software business.

Software revenue actually fell 2% during the quarter to $6.8 billion.

Management says many of Oracle’s largest cloud contracts are prepaid or use equipment provided by customers, which should help protect margins. The company also believes its cloud business can eventually produce returns in the high-20% range.

Oracle is still expecting strong growth. Revenue is projected to rise 27% to 29% in the first quarter.

|

Maria’s Bottom Line This is starting to sound familiar. A company reports strong earnings, huge AI demand and a growing backlog. Then the stock drops because investors are worried about spending, margins and cash flow. Oracle’s business is clearly growing. The question is no longer whether customers want its AI infrastructure. The question is how much Oracle has to spend to deliver it—and how long investors must wait before that spending turns into real free cash flow. Same story, different stock: great growth, huge AI spending and a market that wants to see the profits. |

Educational only. Investing involves risk.

|

Apply to The AI Trading Institute Learn How We Actually Build, Run, and Update Our AI Trading Robot PhilThe next class starts Monday, June 29. The waitlist closes Monday, June 15, 2026, at 5:00 PM Eastern Time — just 4 days away. Seats are limited and the group is curated. Rob reviews every application personally and does a personal interview with every applicant. APPLY AT MATHMAKESMONEY.COM → |

» Story No. 2 of 2 · AI Memory · MU Explainer

Tap the image to view full size

Nvidia Gets the Headlines. Memory May Get the Profits.

|

Big Picture: AI is not just a GPU story anymore. It is becoming a memory story — and that puts Micron right in the middle of the trade. |

Everyone talks about Nvidia when they talk about AI.

That makes sense. Nvidia’s GPUs are powering the AI data centers behind OpenAI, Anthropic, Google, Meta, xAI, and nearly every major AI platform.

But the AI boom is not only about GPUs.

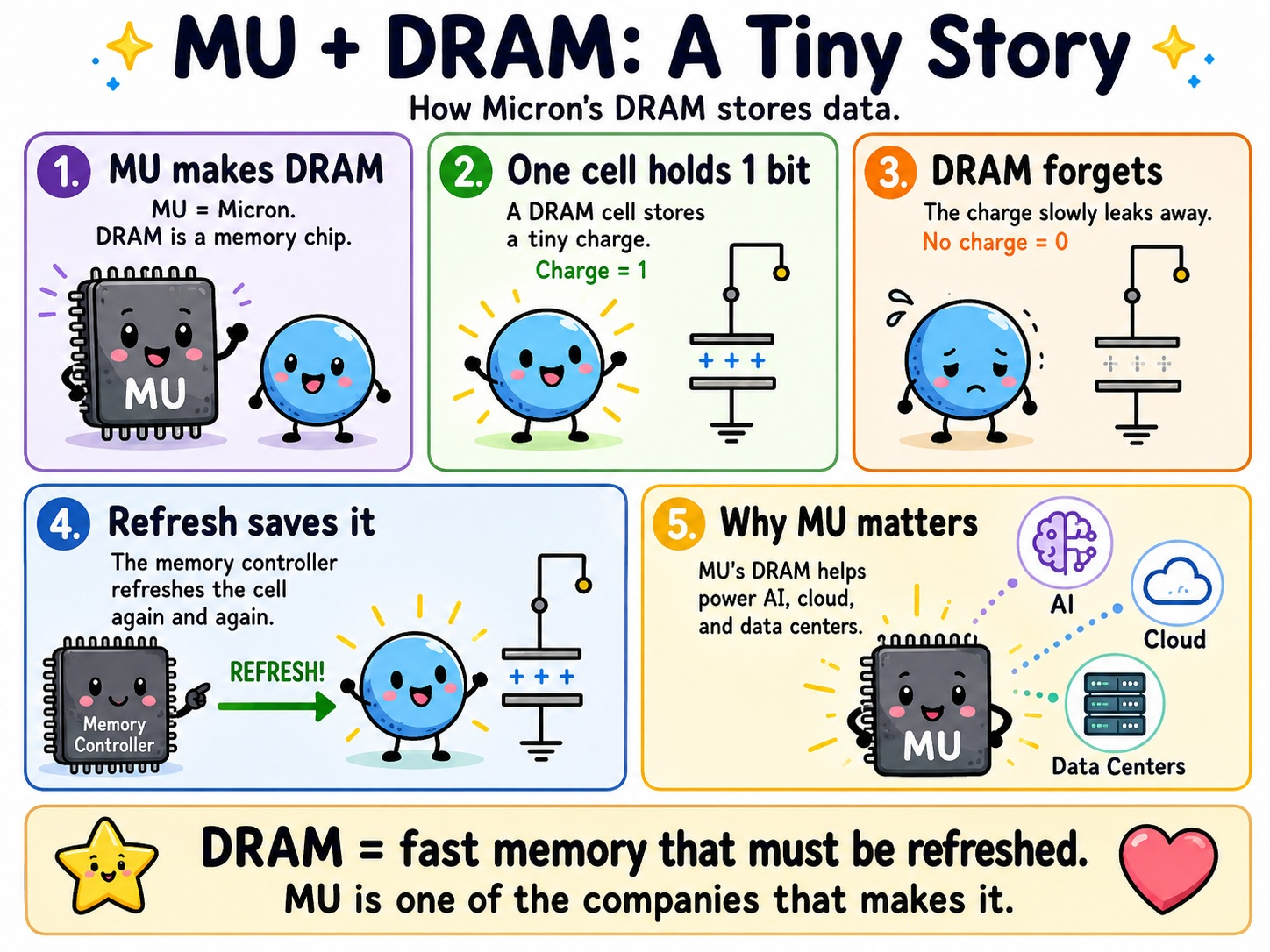

Those chips need massive amounts of memory to work. That is where Micron (MU) comes in.

Micron makes DRAM, which is the short-term memory used inside computers, servers, and AI systems. Think of DRAM as the workspace. The more complex the AI job, the more workspace the system needs.

That is why memory has become one of the most important parts of the AI infrastructure trade.

The Fox Business segment showed DRAM demand projected to grow from roughly 250 exabytes in 2024 to more than 1,200 exabytes by 2031. That is nearly a fivefold increase in seven years.

The key driver is not phones or PCs.

It is data centers.

That matters because AI data centers use far more memory than traditional servers. They need advanced DRAM and high-bandwidth memory to keep the GPUs fed with data. If the memory is not there, the expensive AI chips cannot perform at full speed.

For years, memory was treated like a boom-and-bust commodity business. Prices moved in cycles, supply gluts hurt margins, and investors often avoided the group.

AI may be changing that setup.

If demand keeps rising faster than supply, DRAM prices can stay firm or move higher. For Micron, that is important because stronger memory pricing can flow directly into better margins and stronger earnings.

|

The MU Bull Case: |

The long-term DRAM pricing chart also matters. Historically, DRAM prices trended lower for decades. But recently, pricing has started to turn higher as AI demand absorbs more supply.

That is why Wall Street is starting to look at Micron differently.

This may no longer be just an old-school memory stock. Micron is becoming a direct way to play the AI buildout without buying Nvidia after a massive run.

The big question is whether AI creates a longer and stronger memory cycle than the market is used to seeing. If it does, MU could stay important well beyond one earnings report.

There are still risks.

Memory stocks can move fast. DRAM pricing can turn if supply catches up. Expectations can get too high. Micron can also sell off after earnings even when the long-term story remains intact.

But the big-picture story is clear:

AI does not just need chips.

AI needs memory.

And Micron is one of the companies supplying it.

|

Earnings Watch: Micron reports earnings on June 24. For traders interested in an earnings play, the options chain may be worth watching because premiums are looking attractive. |

Maria’s Take

Micron is not moving because investors suddenly love old-school memory stocks.

It is moving because AI is changing the memory cycle.

If data-center demand keeps growing and DRAM pricing stays firm, MU has a real earnings tailwind. But this is still a cyclical stock, so chasing after a big run can be dangerous.

Micron reports earnings on June 24, so traders looking for an earnings play may want to focus on the option chain instead of chasing shares. Premiums are elevated, and some of the deep out-of-the-money puts are paying well while still sitting far below the current stock price.

Maria’s take: MU stays on the watchlist, but the trade needs discipline. The AI story is real — the risk is paying too much after everyone else finally notices.

Educational only. Not financial advice.

|

Math Makes Money TRADES OF THE WEEK0DTE SPX • $30K SCHWAB ACCOUNT Week of June 11, 2026 |

|

All trades 0dte SPX iron condors on the $30K Schwab account. MEIC = Multiple Entry Iron Condor. 50W = 50-wide wings. 95% = stop loss on short leg. No profit target — let trades expire. |

|

Risk Warning At the time of this writing, we plan on entering most of these trades, but they are part of a much greater and larger trading program and should be considered for educational and entertainment purposes only. Not financial advice of any kind. Trading involves substantial risk and is not suitable for every investor. You can lose some or all of your money. Nothing here is financial advice or a recommendation to buy, sell, or copy any trade. Do not copy trades blindly. Do your own due diligence, understand the risk, and make decisions based on your own account, risk tolerance, and financial situation. |

Join the Live Daily ShowLive trading. Come join us to watch live trading with the AI robot and ask Maria and Rob questions in the chat. A community of trading addicts. JOIN THE TRADING ADDICT → |

|

» Quick Short · Watch on YouTube Today’s 60-Second Recap from Rob ► WATCH ON YOUTUBE

► WATCH ON YOUTUBE

|

Trade small, trade often.

Trade with your head, not with your heart.

Math Makes Money.

Get a fill, Phil.

— Maria

Math Makes Money · AI Trading Holdings LLC