Issue No. 13 • Monday June 8, 2026

|

|

THE TRADING ADDICT

NEWSLETTER

by Maria Helmick

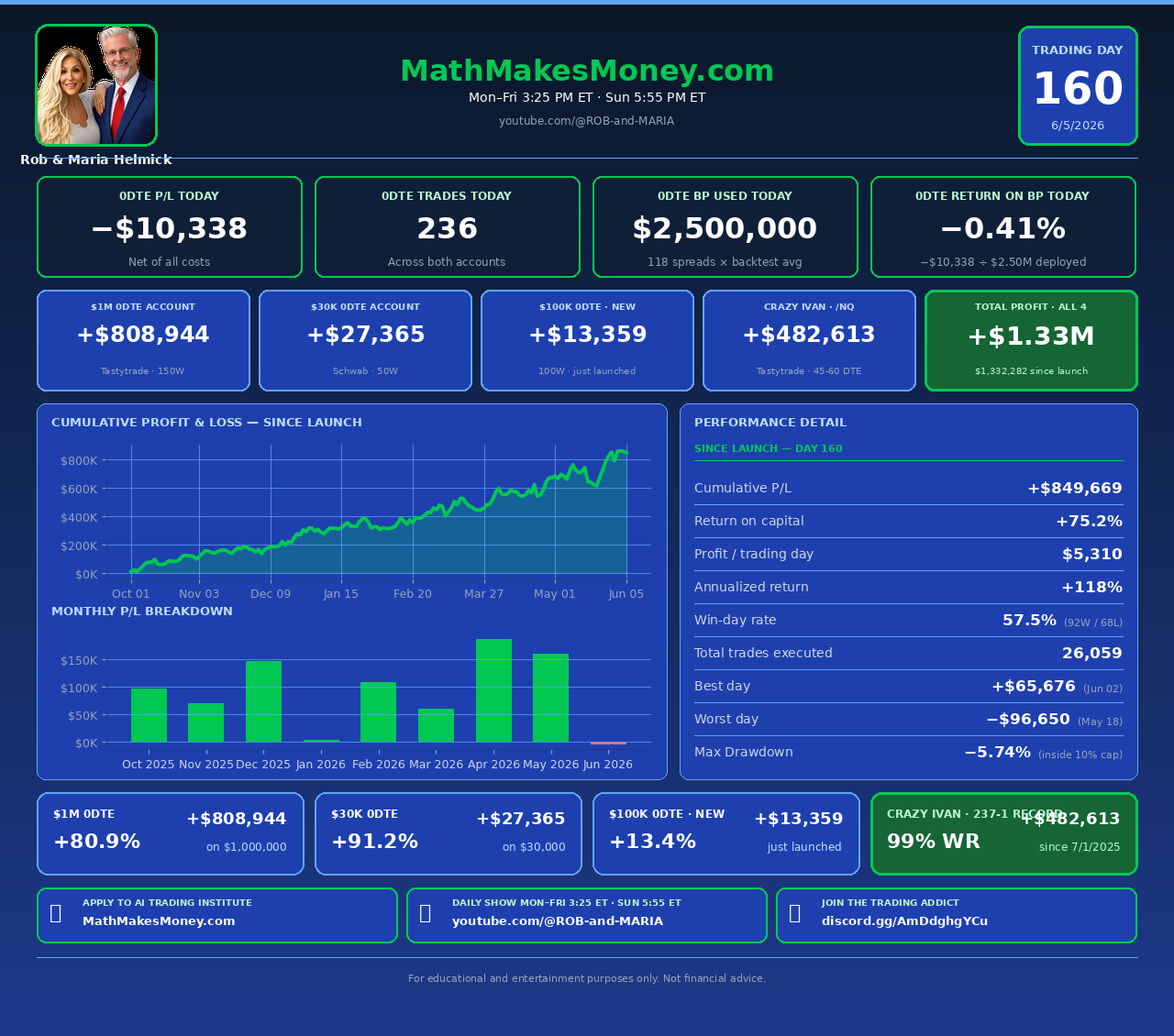

» Daily Trading Update · Day 160 · Tap for live dashboard

Here is how our AI trading robot Phil performed today.

» Trades of the Week are at the end of the Newsletter «

» Story No. 1 of 2 · Market Selloff · What’s Next

Tap the image to view full size

Here We Go…

Hang on to your britches—this week could get bumpy.

Stocks, bonds, gold and Bitcoin were all hit as investors ended the week with very few places to hide.

Friday’s stronger-than-expected jobs report triggered a sharp reversal. The Nasdaq plunged 4.2%, the S&P 500 fell 2.6%, and the Dow dropped 1.3%. It ended the S&P’s nine-week winning streak and erased roughly $1.8 trillion in market value.

The economy added 172,000 jobs in May, about twice what economists expected, while unemployment remained at 4.3%.

Normally, strong employment would be good news. This time, Wall Street saw it differently.

A strong economy gives the Federal Reserve less reason to lower interest rates—and possibly more reason to raise them again if inflation refuses to cool.

Rates Suddenly Matter Again

The two-year Treasury yield climbed to approximately 4.16%, its highest level since February 2025. The 10-year yield moved above 4.5%.

When government bonds begin paying attractive yields, investors have less reason to chase expensive and volatile technology stocks. Higher yields also push up mortgage rates, business borrowing costs and the cost of carrying debt.

The average 30-year mortgage is now around 6.5%, which means the pain is not limited to Wall Street.

The AI Trade Finally Hit a Wall

Semiconductor stocks took the worst beating.

The Philadelphia Semiconductor Index fell more than 10% Friday, wiping out approximately $1.2 trillion in market value. Nvidia, Broadcom, AMD, Micron and other AI-related names were caught in the selling.

But here is the important part: the chip index is still up roughly 73% this year. That tells us how far and how fast these stocks had already climbed.

The AI story may still be real, but expectations became enormous. Investors were pricing in years of explosive growth as though nothing could go wrong.

Friday reminded everyone that when market leadership is concentrated in only a handful of companies, weakness in those companies can quickly drag everything else down with them.

Bridgewater founder Ray Dalio warned that the market’s heavy dependence on one popular and volatile sector looks like the kind of concentration often seen during bubbles. That does not mean AI is finished. It means the easy part of the rally may be over.

There Was Nowhere to Hide

This was not simply money rotating out of technology and into safer investments.

Bonds fell as yields rose. Gold moved near its lowest level of the year. Bitcoin had already been sliding for several days. Investors were pulling money out of several markets at the same time.

That is what made Friday different. It was not just one bad group or one disappointing earnings report. It was a broad reassessment of risk.

Inflation Could Decide What Happens Next

The market’s next major test comes Wednesday at 8:30 a.m. ET, when the May Consumer Price Index is released. Producer inflation follows Thursday morning.

A cooler CPI report could push Treasury yields lower and create a powerful relief rally in technology and semiconductor stocks.

A hotter report could do the opposite. It would strengthen the argument that inflation remains too high and could increase pressure on the Federal Reserve to tighten policy again.

There is no Fed decision this week, but policymakers meet on June 16–17. That makes Wednesday’s CPI and Thursday’s PPI extremely important.

Oil Is Back in the Story

The conflict involving Iran has also put oil and the Strait of Hormuz back at the center of the market.

Any disruption to oil shipments could drive energy prices higher, add to inflation and push bond yields up again.

OPEC+ approved a 188,000-barrel-per-day increase in its July production target. But announcing more production does not guarantee that oil can move smoothly through a region facing military and shipping disruptions.

The dangerous combination for the market would be higher oil, higher Treasury yields and lower technology stocks. That is the mix investors need to watch.

Wall Street Has a New Problem: Too Many Shares

Another challenge is quietly building. The market may soon have to absorb an enormous amount of new stock.

Alphabet announced plans to raise approximately $84.75 billion in equity to help finance its AI ambitions. SpaceX is preparing to raise approximately $75 billion in what could become the largest IPO in history. Anthropic and OpenAI could eventually follow.

These may be exciting companies, but investors do not have unlimited money. To buy newly issued shares, they often have to sell something they already own. That means the flood of IPOs and equity offerings could pull money away from existing technology stocks. The market may love AI—but it still has to pay for all of it.

Oracle and Adobe Get Their Turn

Oracle reports Wednesday after the close, followed by Adobe on Thursday.

Oracle must show that its enormous spending on AI data centers and cloud infrastructure is producing enough revenue to justify the investment.

Adobe must prove that AI is creating real new business rather than simply increasing competition and expenses.

After Friday’s selloff, “good” earnings may not be enough. Investors will be listening closely to guidance, spending plans and what management says about 2027.

Maria’s TakeFriday was more than an ordinary red day. It exposed several risks that had been building beneath the surface: stretched AI valuations, too much dependence on a handful of stocks, rising interest rates and an enormous amount of new stock coming to market. But I am not ready to declare the AI rally dead. The economy is still growing. Chip companies are still making money. And one cooler inflation report could quickly bring buyers back. Watch Treasury yields, oil and the Nasdaq together. If oil and yields rise while technology continues falling, the market may have more pain ahead. If inflation cools and yields retreat, Friday’s damage could set up a strong relief rally. Either way, this does not look like a sleepy week. Hang on to your britches. Here we go… |

Educational only. Not financial advice.

|

Apply to The AI Trading Institute Learn How We Actually Build, Run, and Update Our AI Trading Robot PhilThe next class starts Monday, June 29. The waitlist closes Monday, June 15, 2026, at 5:00 PM Eastern Time — just 7 days away. Seats are limited and the group is curated. Rob reviews every application personally and does a personal interview with every applicant. APPLY AT MATHMAKESMONEY.COM → |

» Story No. 2 of 2 · Risk Management · /NQ Puts

Tap the image to view full size

After a Powerful Run, Is Selling an /NQ Put Worth the Risk?

The Nasdaq’s powerful rally was interrupted by a sharp technology selloff. Rising Treasury yields and changing interest-rate expectations reminded traders how quickly high-valuation technology stocks can reverse.

For put sellers, a decline can create richer premiums and allow strikes to be placed farther below the market. But better premium does not automatically mean better risk.

Is This a Good Environment for Selling Puts?

Possibly. When /NQ falls and volatility rises, option premiums generally become richer. That can allow a trader to sell farther out of the money while still collecting a reasonable credit.

However, one large down day does not mean the market has reached a bottom. Volatility can continue rising, and a short put that initially appears safe can become tested quickly.

Position size matters more than premium.

The Real Risk in an /NQ Put

One /NQ contract moves $20 for every Nasdaq point. A 1,000-point move represents approximately $20,000 per contract.

Your broker may require only a fraction of the contract’s total exposure as buying power, but that margin requirement is not the trade’s true risk. During a sharp decline, losses can increase quickly while volatility and buying-power requirements rise at the same time.

How to Manage Buying Power

For a portfolio concentrated in short /NQ puts, I suggest keeping total buying-power usage at 30% or less.

That leaves at least 70% available to absorb losses, handle higher margin requirements, roll or hedge positions and enter new trades when premiums become richer.

A trader who begins near maximum buying-power usage may quickly lose flexibility if volatility rises or the broker increases margin requirements. The broker’s current requirement should never be confused with the trade’s true risk.

Active Management Is Necessary

Selling naked /NQ puts is not a set-it-and-forget-it strategy. Active management is a necessity.

You must monitor the distance to the short strike, changes in delta and volatility, buying-power expansion and upcoming economic or market events. You should know before entering the trade when you will roll, hedge or reduce the position.

Waiting until the put is deeply tested can make adjustments more expensive and leave fewer choices.

A More Conservative Approach

For traders who decide the premium justifies the risk, a more controlled approach may include:

| • Selling farther out of the money |

| • Using roughly 45 to 75 days until expiration |

| • Targeting approximately the 8-to-12 delta range |

| • Entering smaller positions instead of committing all at once |

| • Taking profits early rather than holding for every dollar |

| • Keeping capital available to roll, hedge or defend the trade |

Scaling into positions can preserve buying power and leave room to take advantage of better premiums if /NQ continues lower.

Rolling Does Not Eliminate the Loss

Most experienced /NQ traders would roll a tested put down and out before accepting an unwanted futures position.

A roll may lower the strike, add time and sometimes generate a credit. But it does not erase the loss. It restructures the position and creates a new obligation.

The account still needs enough liquidity to complete the adjustment, hold the new position and absorb further market weakness.

Defined-Risk Alternatives

Traders who want less exposure can consider a defined-risk put spread, a smaller position, a downside hedge or options on the Micro E-mini Nasdaq-100 contract, which is one-tenth the size of /NQ.

Maria’s Bottom LineSelling naked puts on /NQ is one of my favorite trades, but it is also one of the riskiest. For this strategy, I prefer keeping buying-power usage at 30% or less. That leaves at least 70% available—not because the buying power is being wasted, but because margin can expand quickly when the Nasdaq falls and volatility rises. Active management is not optional. You must watch the position, recognize when risk is increasing and be prepared to roll, hedge or reduce exposure before the account comes under pressure. The premium is the income. Available buying power and active management are the survival plan. |

Educational only. Not financial advice. Futures and naked options can create losses substantially greater than the premium received.

|

Math Makes Money TRADES OF THE WEEK0DTE SPX • $30K SCHWAB ACCOUNT Week of June 8, 2026 |

|

All trades 0dte SPX iron condors on the $30K Schwab account. MEIC = Multiple Entry Iron Condor. 50W = 50-wide wings. 95% = stop loss on short leg. No profit target — let trades expire. |

|

Risk Warning At the time of this writing, we plan on entering most of these trades, but they are part of a much greater and larger trading program and should be considered for educational and entertainment purposes only. Not financial advice of any kind. Trading involves substantial risk and is not suitable for every investor. You can lose some or all of your money. Nothing here is financial advice or a recommendation to buy, sell, or copy any trade. Do not copy trades blindly. Do your own due diligence, understand the risk, and make decisions based on your own account, risk tolerance, and financial situation. |

Join the Live Daily ShowLive trading. Come join us to watch live trading with the AI robot and ask Maria and Rob questions in the chat. A community of trading addicts. JOIN THE TRADING ADDICT → |

|

» Quick Short · Watch on YouTube Today’s 60-Second Recap from Rob ► WATCH ON YOUTUBE

► WATCH ON YOUTUBE

|

Trade small, trade often.

Trade with your head, not with your heart.

Math Makes Money.

Get a fill, Phil.

— Maria

Math Makes Money · AI Trading Holdings LLC